Cartoon Of The Day

Cartoons

Comments Off on Cartoon Of The Day

Jun 042010

This is another in a long line of excellent editorials from Investor’s Business Daily.

Like Jimmy Carter, Obama has the “Midas Touch” in reverse. Except that in Carter’s case it was probably unintentional.

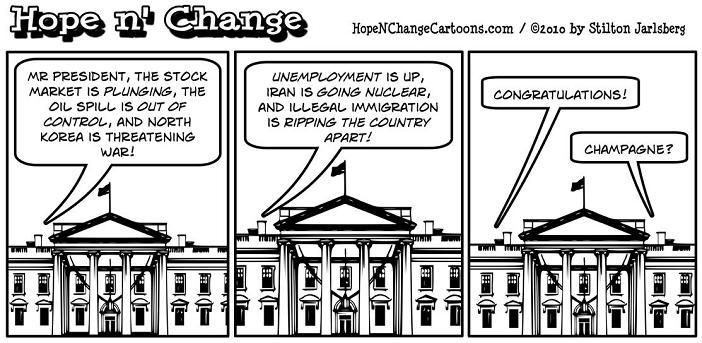

Is It Any Wonder The Market Continues To Sink?

Last Oct. 13, in trying to explain why the market had sold off 30% in six weeks, we acknowledged that the freeze-up of the financial system was a big concern. But we cited three other factors as well:

The imminent election of “the most anti-capitalist politician ever nominated by a major party.”

The possibility of “a filibuster-proof Congress led by politicians who are almost as liberal.”

A “media establishment dedicated to the implementation of a liberal agenda, and the smothering of dissent wherever it arises.”No wonder, we said then, that panic had set in.

Today, as the market continues to sell off and we plumb 12-year lows, we wish we had a different explanation. But it still looks, as we said four months ago, “like the U.S., which built the mightiest, most prosperous economy the world has ever known, is about to turn its back on the free-enterprise system that made it all possible.”

How else would you explain all that’s happened in a few short weeks? How else would you expect the stock market, where millions cast daily votes and which is still the best indicator of what the future holds, to act when:

Newsweek, a prominent national newsweekly, blares from its cover “We Are All Socialists Now,” without a hint of recognition that socialism in its various forms has been repudiated by history as communism’s collapse in the USSR, Eastern Europe and China attest.

Even so, a $787 billion “stimulus,” along with a $700 billion bank bailout, $75 billion to refinance bad mortgages, $50 billion for the automakers, and as much as $2 trillion in loans from the Fed and the Treasury are hardly confidence-builders for our free-enterprise system.

Talk of “nationalizing” U.S.’ troubled major banks comes not just from tarnished Democratic Sen. Chris Dodd, chairman of the Senate Finance Committee, but also from Republicans like Sen. Lindsey Graham of South Carolina and former Fed chief Alan Greenspan.

To be sure, bank shares have plunged along with home prices, and many have inadequate capital. But is nationalization really the only solution for an industry whose main product loans to consumers and businesses has expanded by over 5% annually so far this year?

A stimulus bill laden with huge amounts of spending on pork and special interests is the best our Congress can come up with to get the economy back on track. Economists broadly agree that the legislation has little stimulative power, and in fact will be a drag on economic growth for years to come.

The failure to include any meaningful tax cuts for either individuals or small businesses, the true stimulators of job growth, while throwing hundreds of billions of dollars at profligate state governments and programs such as $4.2 billion for “neighborhood stabilization activities” and $740 million to help viewers switch from analog to digital TV has investors shaking their heads.

A $75 billion bailout for 9 million Americans who face foreclosure, regardless of how they got into financial trouble, is the government’s answer to the housing crunch. Many Americans who have scrupulously kept up with payments are steaming at the thought of subsidizing those who’ve been profligate or irresponsible.

With recent data showing that as much as 55% of those who get foreclosure aid end up defaulting anyway, a signal has been sent that America has gone from being “Land of the Free” to “Bailout Nation.”

Energy solutions ranging from the expansion of offshore drilling and the development of Alaska’s bountiful arctic oil reserves to developing shale oil in America’s Big Sky country, tar-sands crude in Canada and coal that provides half the nation’s electric power, are taken off the table.

The market knows full well what drives the economy and that restraining energy supply will make us all poorer and investing less profitable. Taking domestic energy sources off the table makes us more reliant on sources from hostile and unstable regimes, breeding uncertainty in a capital system in which participants seek stability.

Lawmakers who seem more interested in pleasing special interests than voters back home now control Congress. Some of the leading voices in crafting the massive bank bailout and stimulus packages including Sen. Chris Dodd, Rep. Barney Frank and House Speaker Nancy Pelosi were the very ones who helped get us in this mess.

They did so by loosening Fannie Mae and Freddie Mac’s lending rules and pushing commercial banks to make bad loans. Both Dodd and Frank were recipients of hefty donations from Fannie, Freddie and other financial firms they were charged with regulating.

Trade protectionism passes as policy, even amid the administration’s lip service to free trade. Congress’ vast stimulus bill and its “Buy American” provisions limit spending to U.S.-made products and will drive up costs, limit choices and alienate key allies.

Already, it has triggered rumblings of retaliation in a 1930s-style trade war from trading partners, just as the Smoot-Hawley tariffs prolonged the Great Depression. Several European partners have begun raising barriers. Meanwhile, three signed free-trade pacts with Colombia, Panama and Korea languish with no chance of passage. Free trade offers one way out of our problems, yet it’s been sidetracked.

A 1,000-plus page stimulus bill is bulled through Congress with no GOP input and not a single member of Congress reading it before passage. It borders on censorship.

GOP protests of the bill’s spending and the speed it was passed at were dismissed by Obama and other Democrats as seeking to “do nothing” or “breaking the spirit of bipartisanship.” But voters are angry.

Along with thousands of angry phone calls to Congress, new Facebook groups have emerged, and street protests have sprung up in Denver, Seattle and Mesa, Ariz., against the “porkulus.” CNBC Chicago reporter Rick Santelli’s on-air denunciation of federal bailouts for mortgage deadbeats attracted a record 1.5 million Internet hits.

Business leaders are demonized. Yes, there are bad eggs out there like the Madoffs and Stanfords. But most CEOs are hugely talented, driven, highly intelligent people who make our corporations the most productive in the world and add trillions of dollars of value to our economy.

They don’t deserve to be dragged before Congress, as they have been dozens of times in the past two years, for a ritual heaping of verbal abuse from the very people most responsible for our ills our tragically inept, Democrat-led Congress.

Words like “catastrophe,” “crisis” and “depression” are coming from the mouth of the newly elected president, rather than words of hope and optimism. Instead of talking up America’s capabilities and prospects, he talks them down the exact opposite of our most successful recent president, Ronald Reagan, who came in vowing to restore that “shining city on a hill.”

Even ex-President Clinton admonished Obama to return to his previous optimism, saying he would “just like him to end by saying that he is hopeful and completely convinced we’re gonna come through this.”

The missile defense system that brought the Soviet Union to its knees, and which offers so much hope for future security, is being discussed as a “bargaining chip” with Russia. This, at the same time the regime in Iran is close to having a nuclear weapon and North Korea is readying an intermediate-range missile that can reach the U.S.

This sends a message of weakness abroad and contributes to a feeling of vulnerability at home. A strong economy begins and ends with a strong defense.

All this in barely a month’s time. And to think that more of the same is on the way seems to be sinking in. Investors are watching closely and not caring for what they see. Sooner or later, the market will rally but not without good reason to do so.